From Policy to Profit: The New Era of Out-of-App Game Monetization

Words by Liz Adam, VP, Corporate Affairs

Mar 04 2026

5 mins

This week at the Game Developers Conference (GDC) in San Francisco, thousands of game developers and publishers will gather to discuss the future of games. One of the most crucial shifts is happening in the monetization and distribution space outside primary app stores.

That shift accelerated on 4 March 2026, when Google announced major changes to Android following its global settlement with Epic Games. Google is introducing more billing flexibility, lower Play Store fees, and an optional Registered App Stores program to make it easier to install approved third-party app stores. Epic CEO Tim Sweeney also said Fortnite will return to Google Play globally.

For game publishers, this matters because it expands the routes to monetization beyond traditional in-app purchases. App stores still matter. But they are no longer the only path to revenue, and publishers now have more room to connect in-game experiences with web stores, alternative payments, and other direct-to-consumer channels.

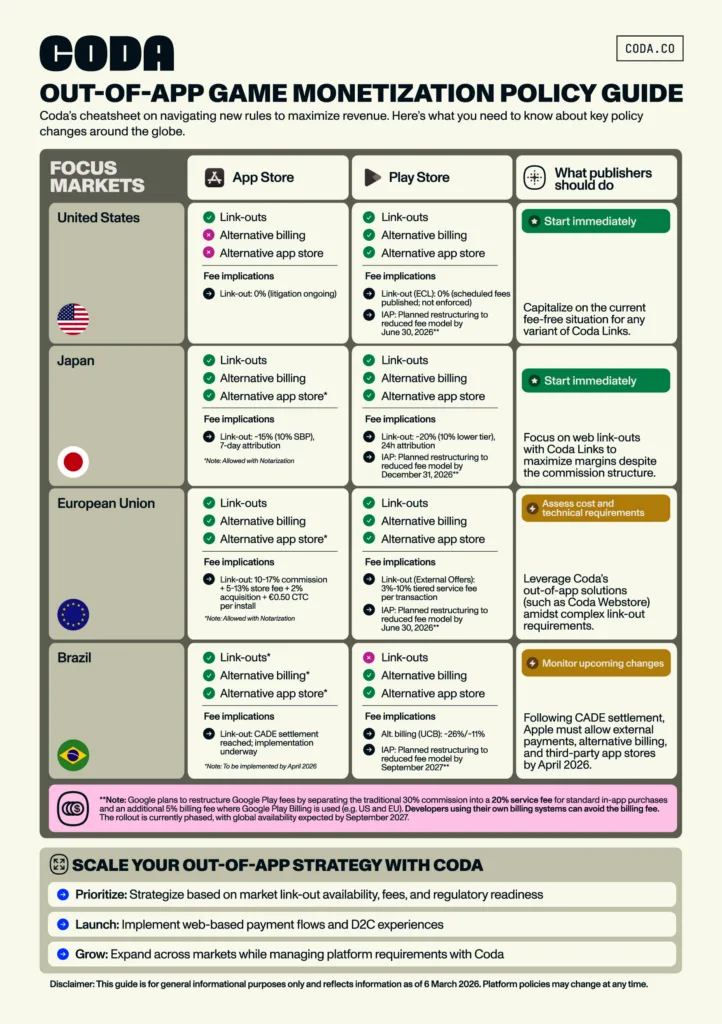

The opportunity is growing quickly. The rules, however, vary widely by market.

To help publishers navigate this landscape, we developed the Out-of-App Game Monetization Policy Guide, a snapshot of the latest policy developments across major markets.

The Global Shift Underway

Across several major jurisdictions, governments and courts are reshaping how digital platforms operate.

In the United States, Google’s current injunction-era framework still allows alternative billing with no platform fee for now, pending a further court hearing. At the same time, Google and Epic have proposed a broader settlement that would replace that structure with a new global-style model if approved.

In Japan, the new Mobile Software Competition Act will require Apple and Google to allow alternative billing systems, link-outs, and third-party app marketplaces.

In the European Union, the Digital Markets Act requires large platforms to allow external purchasing links and alternative app distribution paths, although the associated fees and technical requirements remain complex.

In Brazil, competition authorities have also moved to expand alternative billing and third-party store options.

Taken together, these developments signal a clear shift. Publishers now have more ways to reach players and process transactions outside traditional app store payment systems.

| Key terms: Out-of-app monetization:Revenue generated outside primary app store billing systems, typically through web stores, external payment links, or alternative purchase flows. Link-out:A mechanism that directs users from an app to an external website where purchases can be completed outside platform billing systems. Alternative billing: A framework allowing developers to offer payment methods other than the platform’s native billing system, including models such as User Choice Billing (UCB). Third-party app marketplace: An app distribution channel operated independently from primary app stores such as App Store or Google Play. Direct-to-consumer (D2C): A commercial model where publishers sell directly to players through owned channels such as web storefronts. |

What Changed on Android

Google’s latest update matters because it goes beyond a headline fee cut.

Google says developers will be able to use their own billing systems inside apps alongside Google Play Billing, or guide users outside the app to their own websites for purchases. Google is also introducing a Registered App Stores program for approved third-party app stores, beginning outside the US first, subject to court approval where relevant.

Google is also restructuring Play Store economics. For new installs, Google says the standard in-app purchase service fee will be 20%, with an additional 5% billing fee in the US, UK, and EEA if developers use Google Play Billing. Google also says recurring subscriptions will carry a 10% service fee. Rollout begins by 30 June 2026 in the US, UK, and EEA, then Australia by 30 September, Japan and Korea by 31 December, and the rest of the world by September 2027.

The latest Google–Epic news also matters symbolically. Fortnite’s return to Google Play marks the end of one of the industry’s most visible platform disputes and signals that Android is entering a more open commercial phase. For publishers, that is not just legal housekeeping. It is a sign that out-of-app monetization is becoming a mainstream strategic consideration.

Why Direct-to-Consumer Matters

Out-of-app monetization is not only a policy story. It reflects how digital commerce is evolving.

Players increasingly expect flexible payment options. In many regions, local payment methods such as e-wallets, carrier billing, and real-time bank transfers dominate over credit cards.

Direct-to-consumer commerce allows publishers to reach players through the payment methods they already use. It also allows publishers to run targeted promotions, offer tailored pricing, and build direct relationships with players.

For most publishers, this approach complements rather than replaces app store distribution. The objective is to expand the commercial surface around the game.

What Publishers Should Do Now

The opportunity is real, but execution requires discipline. Three priorities stand out.

- Start with markets where link-outs are clearly permitted.

Markets such as the United States and Japan currently offer the most immediate opportunities.

- Prioritize payment localization.

Access to local payment methods is often the single biggest driver of conversion outside app stores.

- Build scalable web commerce infrastructure.

Direct-to-consumer strategies require robust storefronts, payment orchestration, fraud management, and compliance across multiple jurisdictions.

The Next Phase of Game Monetization

At GDC this year, the conversation around out-of-app monetization has shifted from theory to execution.

Policy change has opened the door. The next phase will be led by publishers that translate these changes into scalable commercial strategies across markets.

The future of game monetization will not happen in one place.

It will happen across a broader digital commerce ecosystem.

Meet us at GDC: https://www.coda.co/events/gdc-2026/

Mar 06 2026

6 mins

Feb 26 2026

3 mins

Feb 23 2026

4 mins

Feb 13 2026

4 mins

© 2026 Coda Payments Pte. Ltd

Site Credits